Being compliant with regulatory requirements is only one reason to have an audit. There are also a number of benefits to having your financial statements audited by Loucas.

The Audit Process

As part of the audit process, we will review and test your accounting systems and controls that you have in place and identify any weaknesses. We will sit down with you and discuss these whilst also suggesting useful improvements to ensure a robust internal control environment.

The benefits of having an audit

Regular audits can help deter fraud from occurring. Our audit tests are designed to reduce the risk of fraud and error within the company.

An audit can help provide assurance to directors and shareholders who may not be involved heavily in the day-to-day running of the company.

An audit can also help provide assurance to bank and lenders

(current and prospective).

Loucas will provide advisory services to you that can benefit management and those charged with governance. Such advice would include but isn’t restricted to, tightening internal controls, reducing the risk of fraud, tax planning, technical advice, how the business is running and what can be achieved.

An audit can enhance the credibility of the financial statements for various third parties:

Audited accounts can help with credit ratings

Suppliers can favour audited accounts when considering credit risk

HMRC when placing reliance on the accounts

Investors (current and prospective)

How we can help

At Loucas, we understand that you would like peace of mind knowing that your financial statements are in full compliance with statutory requirements. To find out more, call us on 01622 758257and speak to one of our audit experts.

2021 will see the UK host COP26, where parties from around the world will gather together to find ways to work towards the goal of a low-carbon future.

The UK government itself must accelerate the reduction of carbon emissions in order to hit the country’s climate target by 2050. The desire to reach these goals has been further fuelled by the coronavirus (COVID-19) pandemic, with many people urging governments to ‘build back better’ and businesses assessing their own roles in the ‘Green Industrial Revolution’.

For this to happen, the government will need to deliver fundamental change to help the UK meet its net-zero target while aiding an economic recovery. Chancellor Rishi Sunak has already laid out some steps towards creating a greener economy. Here, we take a look at what could be done to drive these ambitions further.

Committing to green growth

In the 2021 Budget, the Chancellor made a number of commitments to green growth. This included the first ever UK Infrastructure Bank, which will have an initial capitalisation of £12 billion and will invest in green public and private projects.

The Chancellor also unveiled a retail savings product to give UK savers the chance to support green projects to sit alongside a Sovereign Green Bond that was announced last year. Mr Sunak also committed investment to offshore wind, with funding for new port infrastructure to build the next generation of projects in Teesside and Humberside.

Holistic plan

The Confederation of British Industry (CBI) has urged the government to go further in order to encourage the green industrial revolution. It says that greening the tax system must go beyond simply looking at different environmental taxes – transport, pollution and energy taxes – as one-offs. Instead it should deliver fundamental change with a holistic, coherent tax plan to help the UK meet its net-zero target.

Bumps in the road

However, the UK government has also come in for criticism for cutting electric vehicle grants by £500 while continuing to freeze fuel duties of petrol and diesel vehicles. The Department for Transport will now provide grants of up to £2,500 for electric vehicles on cars priced under £35,000. This is a reduction from the previous £3,000 available for vehicles costing up to £50,000.

The government says this means the funding will last longer and be available to more drivers. However, critics say the cut in grants sends the wrong message, while the fuel duty freeze highlights the challenge facing the government as it seeks to assist the post-COVID recovery whilst also building back better.

How we can help

We aren’t just your average accountants. We offer a wide range of business advisory services to help you make the right decisions for your business to grow and improve. With over 40 years experience our team is dedicated to really understanding your business.

We believe by staying up to date with not only current but changing legislation and industry news we are better placed to help our clients and their businesses succeed.

If you would like to know how Loucas can assist you please do not hesitate to contact us.

If you fail to carry out checks on suppliers of labour to your business, you could become liable for unpaid National Insurance Contributions and denied input VAT claims.

HMRC expect businesses to carry out adequate checks on their suppliers to allow them to make informed decisions as to their integrity.

HMRC’s guidance on the matter is based around three principals: Check – Know your own risk – legal, financial, tax and social obligations, and those of your suppliers. Act – Carry out robust due diligence on your suppliers. If risks are identified do not ignore them, act to mitigate or remove the risk completely. Review – Effective due diligence needs continuous monitoring and review.

HMRC have recently updated their extensive guidance on their website to assist businesses in following these three principals. It could prove very costly for businesses that fail to meet these obligations, as should HMRC look to recover unpaid taxes from the business, the amounts involved are likely to be very large. It is also possible that HMRC would seek to impose a penalty and fine.

How we can help

We aren’t just your average accountants. We offer a wide range of business advisory services to help you make the right decisions for your business to grow and improve. With over 40 years experience our team is dedicated to really understanding your business. We believe by staying up to date with not only current but changing legislation and industry news we are better placed to help our clients and their businesses succeed.

If you would like to know how Loucas can assist you please do not hesitate to contact us.

The Good Work Plan is the Governments response to the Taylor Review of Modern Working Practices in the UK.

What is the Good Work Plan?

From 6th April 2020, The Good Work Plan attempts to provide better clarity on employment rights and ensure individuals are well informed.

The changes implemented by the Good Work Plan are listed as

follows:

Employment Status

Holiday pay

Written Statement for Employment Rights

Agency workers

Extra Protection from redundancy for pregnant

woman and new parents

Stable contracts vs zero hours contracts

Written Statement for Employment Rights

There are a series of changes to the contract of employment which came to effect in 6th April 2020. The new requirement is to provide all employees and workers with a Written Statement of the main Terms and Conditions of Employment on or before the first day of work.

It is important that employers have the contracts prepared

in advance of the start date, preferably at the point of offer. The information

to be included is as follows:

Changes to Contract of Employment

how long a job is expected to last, or the end date of a fixed-term contract

the notice to be given by employer and worker to terminate the agreement

details of eligibility for sick leave and pay

details of other types of paid leave e.g. maternity leave and paternity leave

the length of any probationary period and any specific conditions

all remuneration (not just pay) e.g. vouchers, lunch, health insurance, child care vouchers.

the normal working hours, the days of the week the worker is required to work, and whether or not such hours or days may be variable, and if they may be how they vary or how that variation is to be determined

details of any training entitlement given by the employer and whether any part of that training is mandatory and details of who will pay for any training;

If you hold shares in

a company that have become of negligible value, even if you have not yet

disposed of them, it is possible to make a negligible value claim and

potentially reduce your tax liability.

If such a claim is

made, you will be treated as if you have sold the shares and immediately

required them back at their value at that time.

This effectively crystallises the loss.

Although negligible value is not defined by law, HMRC’s guidance states “An asset is of negligible value if it is worth next to nothing”

You must own the shares at the time of making the claim. If a company has been dissolved the shares no longer exist and therefore it would be too late to make a claim. The timing of a claim is therefore particularly important, so any opportunity is not lost.

How can these losses

be used to save tax?

The loss can be set

off against other capital gains you have made in that year. If certain conditions are met, it is also

possible to backdate the claim to the previous two tax years. Any unused losses can be carried forward to

future years.

Perhaps more useful, in certain circumstances, it is possible to set the loss off against other income as opposed to just other capital gains.

The relief must be

claimed within one year of the 31 January after the tax year in which the claim

is made.

For the shares to

qualify, they must have been subscribed for in a qualifying company. Broadly speaking, for the company to qualify it

must meet similar conditions as to those of an Enterprise Investment Scheme (“EIS”)

qualifying company. These are smaller

companies not listed on a stock exchange.

Furthermore, the

company must have been trading for a period of six years up to the date of

disposal or its entire existence if that is less. Although, if the company did

stop trading before the disposal the company may still qualify under certain

conditions.

It is possible to

set the loss off against income in the year of the claim, the preceding year or

both years. A slight downside is that

the loss can not be restricted in any year to preserve personal allowances, so

care needs to be taken to ensure the loss is utilised in the most effective way.

Unless the shares have been acquired via SEIS or EIS then any loss claim is restricted to £50,000 or 25% of that year’s income whichever is greater.

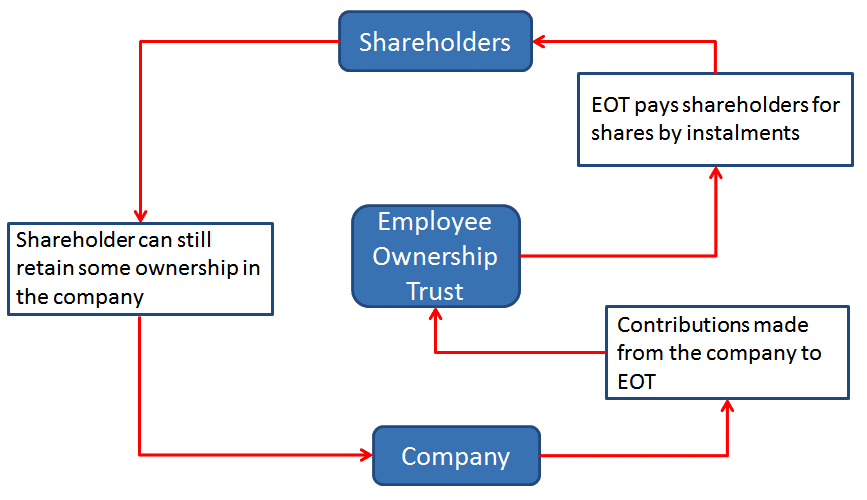

Employee Ownership Trusts (“EOT”) were first introduced in 2014 to facilitate more businesses being wholly or partly owned by employees.

There are some generous tax breaks on offer to encourage business owners to consider the EOT model.

What actually is an EOT?

A trust is set up which will hold all or some of the shares in the company. In order to benefit from the tax breaks the trust must own more than 50% of the shares in the company.

The trust will be operated for the benefit of the employees of the company. The trust is run by its trustees, which could include members of the management team, but given that its purpose is to hold the directors to account, it should be sufficiently independent to enable it to do this. It is necessary to demonstrate to HM Revenue & Customs that control of the business has passed to the EOT and having the trustees dominated by the original shareholders /directors would make this very difficult.

Employee Ownership Trust Model

How does it work in practice?

For new businesses, the EOT model could be put in place from the outset. For existing businesses, the shareholders would sell all or some of their shares to the EOT.

An independent market rate valuation of the business should be obtained which would set the sale price of the shares.

The company would make a contribution to the trust enabling it to pay for the shares. Depending on the funds available, a loan may have to remain between the trust and sellers which would be repaid over a period of time as the company generates future profits.

It may be possible for the company /trust to raise finance to help pay for the shares over a shorter period. The original business owners, post disposal, are able to retain some ownership in the business, keep their posts as directors and also receive market rate remuneration packages.

The company will continue to be run by the management team on a day to day basis, although they will now be answerable to the trustees of the EOT.

Tax breaks

Shareholders are able to sell their shares to the EOT free of Capital Gains Tax. With the recent reduction in Entrepreneur’s Relief this is even more attractive.

Income tax free bonuses of up to £3,600 per year can be paid to each employee.

What are the benefits of an EOT?

There are a number of benefits for the different business stakeholders.

Existing Business Owners

Capital Gains Tax free

Ready and willing buyer for the business

Reassurance that the business will continue as a going concern

Able to retain some ownership in the business

Employees

Tax free bonuses

A sense of ownership

The Company

An engaged workforce

Ensured long term future

Can continue with minimal disruption

A more innovative and forward thinking culture

The employee ownership model may not be suitable for all businesses, but it is fast becoming a popular choice for businesses who recognise the value of their most important resource.

An EOT is just one type of employee ownership model and other options such as share schemes should also be considered.

Disclaimer: Content posted is for informational & knowledge sharing purposes only, and is not intended to be a substitute for professional advice related to tax, finance or accounting. Each comment posted by third party readers/subscribers of our website on topics of tax and accounting is their personal opinion and due professional care should be taken by you before you act after reading the contents of that post. No warranty whatsoever is made that any of the posts are accurate and is not intended to provide, and should not be relied on for tax or accounting advice.

The

VAT payment deferral period, which was introduced as a measure to ease

financial pressure on businesses during the COVID-19 pandemic, ends on 30 June

2020. Any liabilities that fall due on or after 1 July 2020 should be

paid in full by the due date, unless there is a time to pay arrangement in

place.

Businesses

will need to consider setting up any cancelled direct debits in enough time for

HMRC to take their next VAT payment.

Any deferred VAT payments should be paid in full on or before 31 March 2021. Additional payments can be made with subsequent returns.

Disclaimer: Content posted is for informational & knowledge sharing purposes only, and is not intended to be a substitute for professional advice related to tax, finance or accounting. Each comment posted by third party readers/subscribers of our website on topics of tax and accounting is their personal opinion and due professional care should be taken by you before you act after reading the contents of that post. No warranty whatsoever is made that any of the posts are accurate and is not intended to provide, and should not be relied on for tax or accounting advice.

The

Government have recently issued further guidance on two of the support packages

available to businesses affected by COVID-19.

Coronavirus

Job Retention Scheme (“CJRS”)

The updated guidance on the CJRS sets out the procedures following the changes that come into force on 1 July 2020. The major change on 1 July will be that employers will be able to bring back employees on a part time basis. The guidance covers in detail how the furlough grant should be calculated in this situation.

The

CJRS will come to an end on 31 October with the level of support being reduced

as from 1 August.

June

and July – The level of support is be unchanged

August

– the Government will pay 80% of wages up to a cap of £2,500 and employers will

pay ER NICs and pension contributions for the hours the employee does not work.

September,

the Government will pay 70% of wages up to a cap of £2,187.50 for the hours the

employee does not work. Employers will pay ER NICs and pension contributions

and 10% of wages to make up 80% total up to a cap of £2,500.

October,

the Government will pay 60% of wages up to a cap of £1,875 for the hours the

employee does not work. Employers will pay ER NICs and pension contributions

and 20% of wages to make up 80% total up to a cap of £2,500.

Self-Employment

Income Support Scheme (“SEISS”)

The

deadline for claiming the first grant under the SEISS is 13 July. All

claims must be made on or before this date. To find out if you are

eligible to make a claim follow this link.

Details of the second and final grant for self employed individuals have been released on the .GOV website. Eligible individuals can claim a taxable grant worth 70% of their average monthly trading profits, paid out in a single instalment covering three months’ worth of profit, and capped at £6,570 in total.

The

eligibility criteria are the same for both grants, and individuals will need to

confirm that their business has been adversely affected by coronavirus when

applying for the second and final grant. An individual does not need to have

claimed the first grant in order to be eligible for the second and final grant.

Applications to make a claim for the second grant will open in August 2020.

Disclaimer: Content posted is for informational & knowledge sharing purposes only, and is not intended to be a substitute for professional advice related to tax, finance or accounting. Each comment posted by third party readers/subscribers of our website on topics of tax and accounting is their personal opinion and due professional care should be taken by you before you act after reading the contents of that post. No warranty whatsoever is made that any of the posts are accurate and is not intended to provide, and should not be relied on for tax or accounting advice.

HMRC have announced a five month delay to the introduction of the VAT Domestic Reverse Charge.

The significant changes to how VAT is applied to services in the construction industry will now not come into force until 1 March 2021.

The

delay will no doubt be a relief for many construction businesses who are

already having to deal with the uncertainty caused by the COVID-19 pandemic.

You can read the full guidance regarding these changes on HMRC’s website.

Disclaimer: Content posted is for informational & knowledge sharing purposes only, and is not intended to be a substitute for professional advice related to tax, finance or accounting. Each comment posted by third party readers/subscribers of our website on topics of tax and accounting is their personal opinion and due professional care should be taken by you before you act after reading the contents of that post. No warranty whatsoever is made that any of the posts are accurate and is not intended to provide, and should not be relied on for tax or accounting advice.

In

an attempt to help businesses that were unable to access funds through the

Coronavirus Business Interruption Loans (CBILS), the treasury recently

announced the Bounce Back Loan Scheme (BBLS).

The terms of these loans have now been confirmed as follows:

Loans

range from £2,000 up to 25% of a business’ turnover to a maximum of £50,000

100%

Government backed loan with no other security required

The

loans are for a period of six years

There

are no interest charges or repayments due in the first year

A

low interest rate of 2.5%

No

early repayment charges

No

arrangement fees

To

be eligible for the BBLS, in general terms, you need to be a business in the

UK, have been affected by Coronavirus and not using CBILS.

Why consider taking out a Bounce Back Loan?

Cash flow

A Bounce Back loan would provide cheap

working capital for your business.

Repayment of existing borrowings

Perhaps consider whether you have any current

business borrowings such as hire purchase agreements, bank loans and overdrafts

or credit card debt that could be settled by using the funds raised from a

Bounce Back loan. It would be important to check that there are no early

repayment charges on existing agreements before doing this.

Funding of capital expenditure

If you are considering investing in new equipment for your business, a BBLS loan could be a more attractive alternative to traditional business borrowing options.

Although

at the time of writing it has not been announced how long the BBLS or CBILS

will be available, it is unlikely that it will be indefinitely and therefore it

is sensible to consider this sooner rather than later.

You can find more details on the Bounce Back loans and indeed the larger Coronavirus Business Interruption Loans on the British Bank Website.

Disclaimer: Content posted is for informational & knowledge sharing purposes only, and is not intended to be a substitute for professional advice related to tax, finance or accounting. Each comment posted by third party readers/subscribers of our website on topics of tax and accounting is their personal opinion and due professional care should be taken by you before you act after reading the contents of that post. No warranty whatsoever is made that any of the posts are accurate and is not intended to provide, and should not be relied on for tax or accounting advice.

HM Revenue & Customs have today released a guide detailing how it will assess eligibility for the Self Employment Income Support Scheme for sole trader businesses that have been affected by COVID-19.

The guide sets out how the profits will be calculated, on which the grant will be based. There are no real surprises, although it is worth noting:

Losses brought forward are not taken into consideration

Capital allowances will be taken into account

The fact that capital allowances are taken into account could mean that for those which purchased a large item of equipment, such as a new van, and have taken advantage of the Annual Investment Allowance will be disadvantaged as their profits will be much lower and therefore will impact the grant they are entitled to. In certain circumstances, it could also mean they are not eligible for the scheme at all.

You can find the full guide by following the link below.

We are registered as auditors and regulated for a range of investment business activities in the United Kingdom by the Association of Chartered Certified Accountants – the global body for professional accountants.

Register to receive our monthly Newswire once a month and we'll send you an email packed full of essential business news and handy tax tips to

help save you money.